Online Banking Login

Online Banking Login

Get Our App:

Enjoy powerful protections and everyday perks with PremiumSpend checking, including identity protection, cell phone coverage, roadside assistance, savings, and more, all at no additional cost.

Finance eligible home energy improvements, including heating and cooling, solar, insulation, EV charging and more with a GoGreen Loan.

Discover special offers, tools and financial solutions curated just for Trojans, quickly and easily in the Trojan Hub.

Join our monthly Member Orientation webinars to discover member benefits, helpful services and special promotions to make the most of your membership. Visit our events page to see what’s coming up.

Join our monthly Member Orientation webinars to discover member benefits, helpful services and special promotions to make the most of your membership. Visit our events page to see what’s coming up.

Enjoy powerful protections and everyday perks with PremiumSpend checking, including identity protection, cell phone coverage, roadside assistance, savings, and more, all at no additional cost.

Finance eligible home energy improvements, including heating and cooling, solar, insulation, EV charging and more with a GoGreen Loan.

Discover special offers, tools and financial solutions curated just for Trojans, quickly and easily in the Trojan Hub.

Join our monthly Member Orientation webinars to discover member benefits, helpful services and special promotions to make the most of your membership. Visit our events page to see what’s coming up.

Join our monthly Member Orientation webinars to discover member benefits, helpful services and special promotions to make the most of your membership. Visit our events page to see what’s coming up.

Get Our App:

Get a free financial education on all things personal finance from credit scores and debt consolidation to saving and student loans.

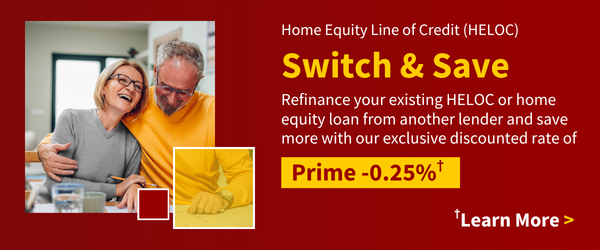

Cash from home equity can go a long way toward a big purchase or one of life’s curveballs. You can tap your home equity for any reason – major renovations or unexpected car repairs, to name two.

|

|

How do HELOCs work? First, since it’s a revolving line of credit based upon the equity you have in your home, you can access the funds as needed over time. Then you pay interest only on the amount you use.

Have a specific purpose for borrowing against your home equity? Consider a fixed-rate home equity loan you repay over time in equal monthly payments, just like a mortgage. This option lets you borrow only as much as you need, perfect for one-time expenses: like covering a tuition payment, paying off high-interest credit cards, or even taking advantage of a real estate investment.

Rates accurate as of 8/8/2026

All rates and terms subject to change without notice.

| Type | APR as low as |

|---|---|

| Interest Only HELOC | 6.65% |

| Traditional HELOC | 6.65% |

*Terms and Conditions: PRIME -0.10% APR disclosure: Annual Percentage Rate (APR) is effective 8.8.2026 variable, and is subject to change. Rate is for combined loan-to-value of 80% or less, owner occupied homes and requires a FICO score of 740+. Higher rates may apply, depending on credit and combined loan-to-value. All loans are subject to credit approval. Credit limits up to $250,000. Appraisal may be required. California properties only. No Annual Fee. Flood and/or property insurance may be required. Your APR can adjust monthly and is based on the Prime Rate as published in the Wall Street Journal. Maximum advance period of 10 years, with a 15-year repayment period. $15,000 minimum initial advance required to avoid a processing fee. Thereafter, minimum advance is $200. Minimum loan balance of $10,000 must be maintained for first 12 months; otherwise, a $500 fee will be assessed. Minimum floor rate of 4.00% APR. Maximum loan rate of 18.00% APR. A sample monthly payment for an interest only HELOC, credit score of 740+ with a balance of $15,000 at 6.65% (Prime -.10%) is $83.13 during the draw period and $131.91 for the repayment period. A sample monthly payment for a traditional HELOC, credit score of 740+ with balance $15,000 at 6.65% (Prime -.10) is $187.50. All Credit Union loan programs, rates, terms and conditions are subject to change at any time without notice. NMLS #448984

Give us a call at 213-821-7100, schedule an appointment, or fill out the form below and we’ll connect you with our team of mortgage specialists!

Unlock the power of your home! Use this simple calculator to estimate how much you can borrow.

Manage life’s big expenses and curveballs with a low-rate home equity loan or line of credit.

Great rates on auto loans and HELOC.

As a home buyer, knowing the difference between being pre-qualified and pre-approved is an important step in the mortgage process. Making your decision on which one to choose starts with understanding the definition of each of those terms.

‘Pre-qualified’ and ‘pre-approved’ for a loan – what’s the difference?

USC Credit Union is here to help you feel more confident in today’s real estate market. We’ve helped thousands of our member-owners reach their homeownership goals and we will do the same for you. Download our Free Home Buyer’s Guide and learn about the entire home-buying process.

Free Home Buyers Guide

In buying or selling your home, timing is everything. While there is no one-size-fits-all answer to the best time to sell or buy a home, there are several factors to consider when making your decision.

When is the best time to sell or buy a home?

Buying a home is one of the biggest financial decisions you’ll make in your lifetime. A mortgage is a loan that helps you finance the purchase of a home, and it’s important to understand how it works.

What is a mortgage?

There’s a lot more to homeownership than paying the mortgage loan. Here are eight extra homeownership costs to consider as you plan for your dream home.

8 Unexpected Homeowner Expenses

1Maximum advance period of 10 years, with a 15-year repayment period. $15,000 minimum initial advance required to avoid a processing fee. Thereafter, minimum advance is $200. Minimum loan balance of $10,000 must be maintained for first 12 months; otherwise, a $500 fee will be assessed.

2Limits from $10,000 – $250,000 depending on your combined loan-to-value ratio and credit scores.

Discuss your options over the phone or at a branch.

Send me an email with your questions – I’ll take it from there.

Reach me by phone, Monday through Friday, 8am – 5pm, PT.